Rising Vehicles Production Boosts Contact Adhesives Market

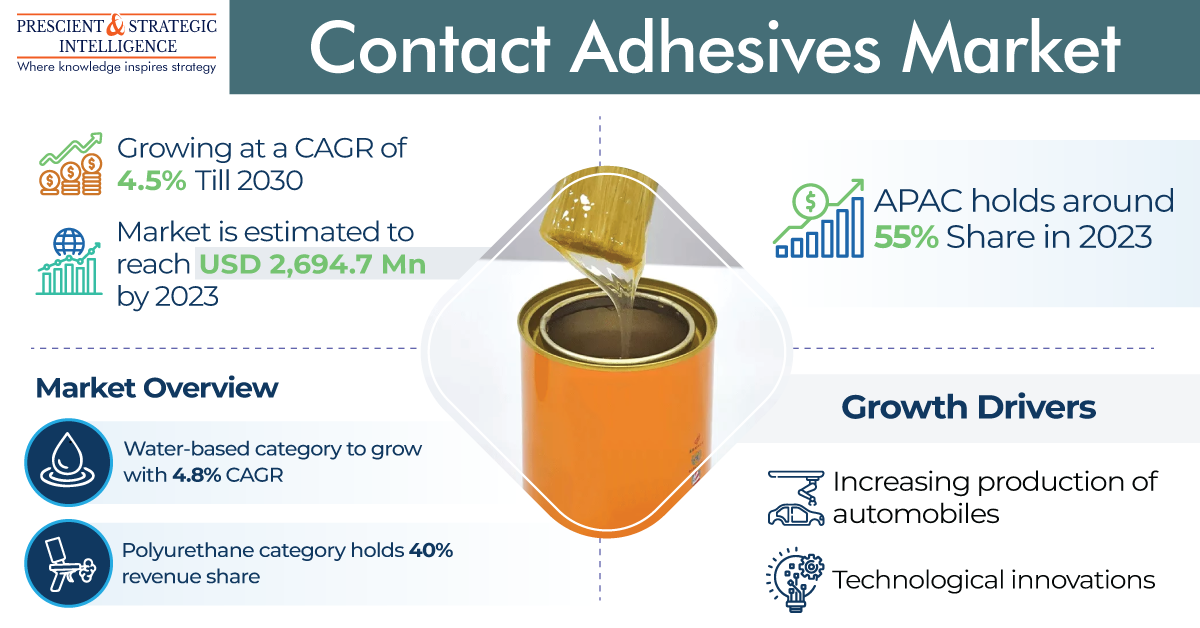

The contact adhesives market was USD 2,694.7 million in 2023, and it will touch USD 3,645.2 million, advancing at a 4.5% compound annual growth rate, by 2030.

The progression in this industry is because of the increasing need for these adhesives in the building and construction sector, coupled with the rising production of vehicles. Also, the leather and footwear sector utilizes them significantly. Moreover, the advancement of technology in these agents in the move toward sustainable practices is also aiding this growth.

The water-based category, based on technology, will propel at the fastest rate, of 4.8%, during this decade. This can be because of the rising need for sustainable products as well as the additional benefits of water-based adhesives compared to solvent-based ones.

The polyurethane category, based on resin type, is leading the industry, with a 40% share, and it is likely to advance at a 4.3% CAGR during this decade. Solvent-based adhesives remain widely employed across different sectors, including woodworking, building and construction, and industrial assembly, because of their exceptional adhesion to various substrates like plastics, metals, fabric, and wood.

The acrylic category is likely to advance at the highest rate, of 5.2%, during this decade. This can be mainly because of the rising need for these types in emerging economies as a result of the ongoing substantial infrastructure expansion.

The construction category, on the basis of end user, was the largest contributor to the contact adhesives market. This is because of the widespread utilization of contact adhesives for various applications in this sector, coupled with its rapid growth in developing nations, including China and India. These adhesives are chiefly employed in fitting roofing, making furniture, and wooden flooring.

Moreover, the automotive category was a significant contributor to the industry. This can be mainly because of the surge in the populace, which boosts the requirements for vehicles. Adhesives are employed to glue separate trim pieces like door panels, headliners, and dashboards, to establish a seamless and smooth finish and enhance stability.

APAC is leading the industry, with a share of 55%, and it is likely to propel at a considerable rate, of 4.7%, in the years to come. This is because of the expanding construction, automotive, packaging, and footwear sectors.

Moreover, India, China, Bangladesh, and Pakistan have significant populations, which results in a high need for all types of products made with these adhesives.

Furthermore, governments are offering help to the manufacturing sector in Indonesia, India, Thailand, and Malaysia. This is resulting in increasing funding as well as production in the automotive sector.

With the surge in the production of vehicles, the contact adhesives industry will continue to progress in the coming years.

Source: P&S Intelligence